Economic Consequences of a Coin Shortage and Cash Hoarding

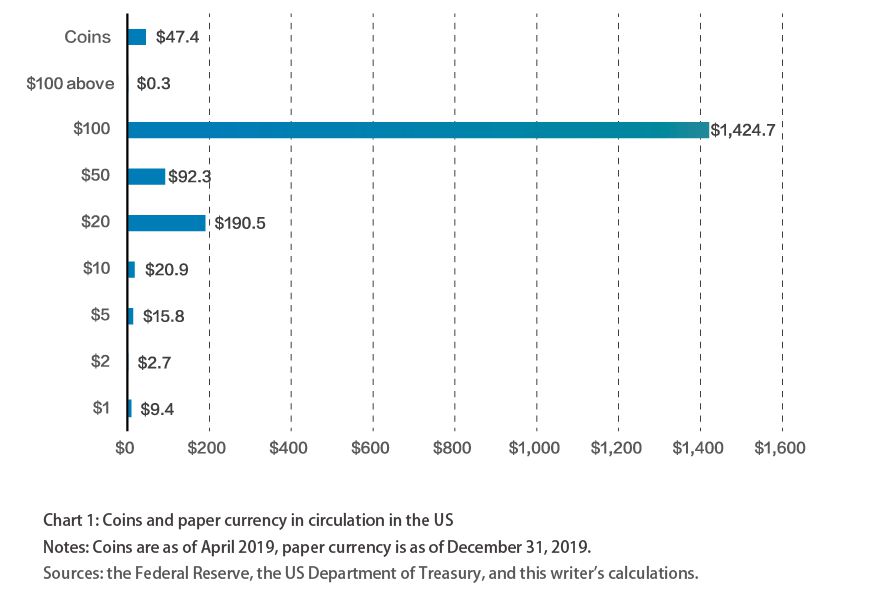

What is a coin shortage? In my view,this is a term that rarely appears in Chinese. In June 2013,there was a "money shortage" in China's financial market,and those who experienced it probably have vivid memories of the unexpected disruptions. In mid-September of 2019,short-term interest rates in the United States suddenly got out of control. This writer once called it an "American-style money shortage." But these terms all refer to the phenomenon of liquidity tension caused by the imbalance of supply and demand for funds or excessive preventive demand,not a shortage of physical currency. In today's era of highly developed payment systems,if someone says that in the world's largest economy with $2 trillion in currency in circulation,suddenly there are not enough coins,you might mistakenly conclude that this could not possibly be true. (For the structure of currency in circulation in the United States,see Chart 1)

But in fact it is true! The first time I heard about this was on the afternoon of June 17,when Fed Chairman Jerome Powell testified before the House Financial Services Committee. During the question and answer segment of the Fed chief's semi-annual remarks on monetary policy,he was asked by Congressman John Rose of Tennessee about a shortage of coins. Rose said that a banker in his state told him the day before that his bank could only get 40% of the coins it sought from the Federal Reserve Bank on a weekly basis. The stock of coins was draining and would soon be exhausted. He asked whether Powell knew.

It is very rare to discuss coin issues at monetary policy hearings. It seems that Powell did not expect this; he was a little surprised by the query. His explanation was: Because the economy is partially closed due to the Covid-19 pandemic,the circulation of coins seems to have stopped,mainly because the places where coins can be exchanged for banknotes are mostly not open. People are unable to exchange unused coins into banknotes,resulting in a decrease in the supply of coins. He emphasized that as the economy gradually opens up,the circulation of coins will improve. He promised that the Fed is working to solve the problem,and the shortage is only temporary.

This question was extremely unusual. Out of curiosity,the author began to follow this clue and found that,in fact,the Federal Reserve issued a notice in June entitled Strategic Distribution of Coin Inventory. This was equivalent to a "temporary coin rationing order." The Fed used to allocate full amounts of coins according to the orders of various commercial banks’but now the Fed had begun distributing coins according to the historical orders of the banks.

The rationing order pointed out the reason for the shortage of coins: the chain of coin production and the normal pattern of coin circulation had been disrupted. Over the past few months’the number of coins deposited by banks in the Federal Reserve Bank has fallen sharply. According to a Fed spokesperson’since March’coin deposits in banks had fallen by about 50% on a year-on-year basis. At the same time’the US Mint had insufficient capacity due to the pandemic. As the economy restarted’coin orders from banks to the Federal Reserve Bank increased’causing federal coin inventories to fall below normal levels.

The announcement also proposed a combination of countermeasures to be taken: allocate inventory more effectively; cooperate with the Mint to minimize supply constraints and maximize coin production; encourage banks to only apply for the number of coins that can meet their customers' recent needs; the inventory can be replenished by relaxing restrictions by banks on depositing coins from customers’including weakening the requirements for loose and rolled coins.

In its statement’the Fed said frankly that although it was confident that once the economy restarted and the coin supply chain returned to normal’the shortage problem would be resolved’but at the same time it was also aware that the above measures alone would not resolve the problem fundamentally in the short term. As the saying goes "distant waters won't quench your immediate thirst."

Congressman Rose also took note of the announcement and criticized the Fed for taking the matter lightly’saying that the guidelines were not strong enough to be reassuring. "Customers go to banks to exchange coins. If they can't get coins’the reaction will be very negative. We don't want to wake up one day and see a headline like this in the newspaper: Banks are out of money!" Rose warned. He also emphasized that it is very important for merchants to have coins for change during the pandemic’because at this time’business is bleak and profits are meager. Whether you can get change often determines whether you make money or lose money.

After the hearing’it was obvious that the Fed and the Treasury Department were under great pressure. On June 30’the Federal Reserve issued another statement’announcing that a "Coin Task Force" would be established in early July’and that strong measures would be taken to solve the problem. The task force has a wide range of members’covering almost all major participants of the coin supply chain’including: the US Mint’which is responsible for production; the Federal Reserve’which is responsible for inventory and distribution; the Armored Carriers’the American Bankers Association’the Independent Community Bankers Association’the National Association of Federal Credit Unions’coin aggregator representatives’and representatives of the largest retail coin users.

The Federal Reserve has emphasized’including in the statement on June 30’that the primary reason for the coin shortage is the rapid slowdown in coin circulation due to the pandemic. For example’the statement stated that according to the forecast of the US Treasury Department’the total value of coins in circulation as of April 2020 was $47.8 billion’which was a slight increase from the $47.4 billion in April 2019. It indicates that there were enough coins in the economy’but the slowdown in circulation has led to a shortage.

The author feels this is a shirking of responsibility. The velocity of circulation is of course the most important factor’but we can't just look for objective reasons. Subjectively’the Fed is somewhat derelict in its duty. The Fed submits orders to the Mint every month and forecasts the demand for coins over the next 12 months. The Mint makes coins based on it the projections. Although coin production is constrained during the pandemic’if the Federal Reserve accurately predicts that bank coin deposits may fall by 50%’the Mint will probably not ignore it. It was obviously too late to organize production after the coin shortage appeared.

In the United States’the recycling of coins is a core element that affects the speed of circulation. There are many types of coin exchange points that can help convert coins into banknotes. For example’there is a company called Coinstar’which operates 18,000 coin exchange machines in the United States. It can exchange $2.7 billion worth of coins into paper money a year. Their coin exchange machine is usually placed in a vending shop. After putting in coins’the machine will spit out a voucher’and you can exchange banknotes directly at the counter of the vending shop with the voucher. But the cost of currency exchange is very high’as much as 11.9% of the coin amount!

Many bank branches can also exchange money. For example’at the Harvard University Employee Credit Union’there is a coin change machine’where members can exchange coins into paper money for free’and non-members are generally charged a fee.

However’during the lockdown’bank lobbies and coin-sorting kiosks in retail stores where coins can be recycled were off limits or saw reduced traffic’thus the flow of coins through the economy kind of stopped.

Although payment methods are becoming more developed now’the coin shortage reminds people that sometimes coins are still necessary. Coins are essential for many payments in the United States’such as parking meters’vending machines’laundromats’playgrounds’and even outdoor campsites for bathing. In contrast’because electronic payment methods are more common in China’there is very little chance of a coin shortage there. With the advent of the digital currency era of the central bank’the demand for physical currency decreases.

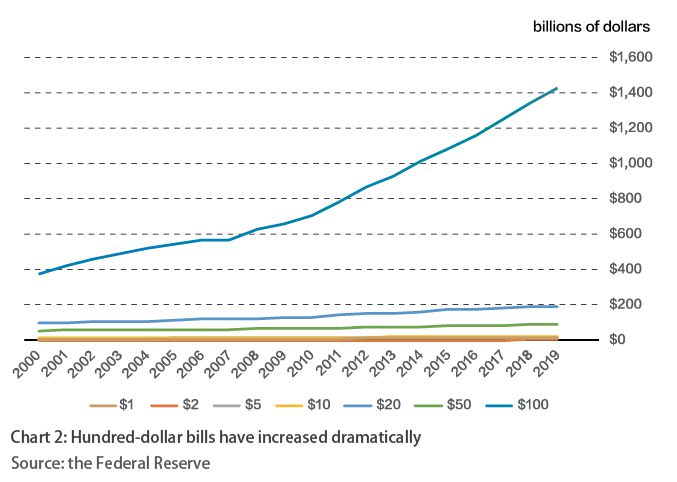

But think about it again; China has 8 trillion yuan in cash’and the US has $2 trillion in currency in circulation’accounting for nearly 10% of their GDP’respectively. In any case’in the foreseeable future’eliminating cash seems unrealistic. It may be necessary to reduce the proportion of large banknotes’as Harvard University professor Kenneth Rogoff suggested in his book The Curse of Cash a few years ago in order to combat tax evasion’corruption’money laundering and even terrorism. What is thought-provoking is that not only has the proportion of US hundred-dollar bills not fallen in recent years’but it has in fact increased dramatically (see Chart 2). The reasons are quite complex’but this is a topic for another day.

Coin shortage vs. cash hoarding

During the early stages of the Covid-19 pandemic’fears that cash might be a virus carrier were widespread. People either reduced the use of cash or used various methods to sterilize the banknotes and coins they handled. In China’the People's Bank of China has required disinfection of used cash since mid-February’ordered the direct destruction of cash recovered from certain industries’released new banknotes as much as possible’and suspended inter-provincial cash transfers. South Korea’Singapore and Thailand have also taken similar measures. In late February’the Federal Reserve quarantined the US dollars shipped from Asia for a period of time before returning them to circulation. What's more’due in part to the vigilance of physical currencies’US coin deposits dropped by 50%’and even retailers had no coins to give customers change. This is evidence of a rare "coin shortage." Even Germany’which is known for its preference for cash’has seen significant growth in its non-cash transactions. Some experts boldly predict that the impact of the pandemic and the advancement of payment methods are leading to the accelerated disappearance of cash’and the era of cashless is coming.

But is cash really disappearing? Reality often deviates from imagination: the actual situation is that in many countries’not only has currency in circulation not decreased’but actually has increased substantially.

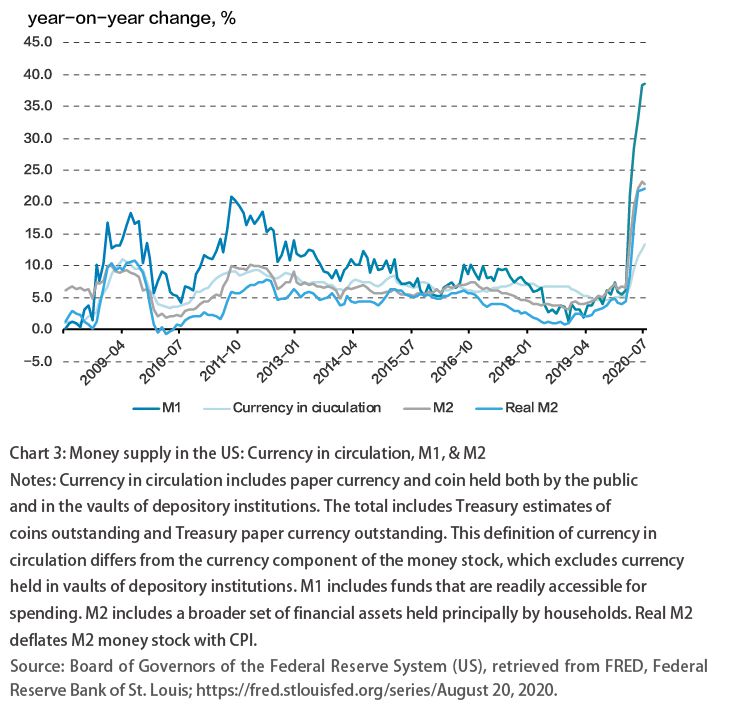

In the US’currency in circulation rose by only $80 billion to $1.8 trillion in 2019. However’the net increase expanded to $180 billion in the first half of 2020’which is more than twice the net increase in all of 2019.

In contrast’as of June’M1’the most liquid portion of money supply’was $5.3 trillion in the US. It grew 39% on a year-over-year basis’which was much higher than the 6.7% rise in February. The stock of M2 as of June was $18.4 trillion’up 24.7% year over year’which was also a relatively high level’but more than 13 percentage points lower than that of M1. (See Chart 3) This shows that the liquidity of money is rising. The same is true in Europe. Recent data from the European Central Bank show that M1 has a year-on-year growth rate of 12.7%’the highest level since 2009 and much higher than the 8.9% year-on-year growth rate of M3. This shows that although people use less cash for transactions but are also hoarding cash.

It's important to note that’in this article’"cash hoarding" refers to the phenomenon that households and businesses hoard the most liquid portion of money supply’which is narrowly defined as currency held by the public(currency in circulation)’and more broadly defined as M1’i.e. the sum of currency in circulation and transaction deposits at depository institutions. In this sense’cash’currency in circulation’and M1 are interchangeable in meaning for most of the time’unless otherwise specified.

Cash Hoarding and Money Supply

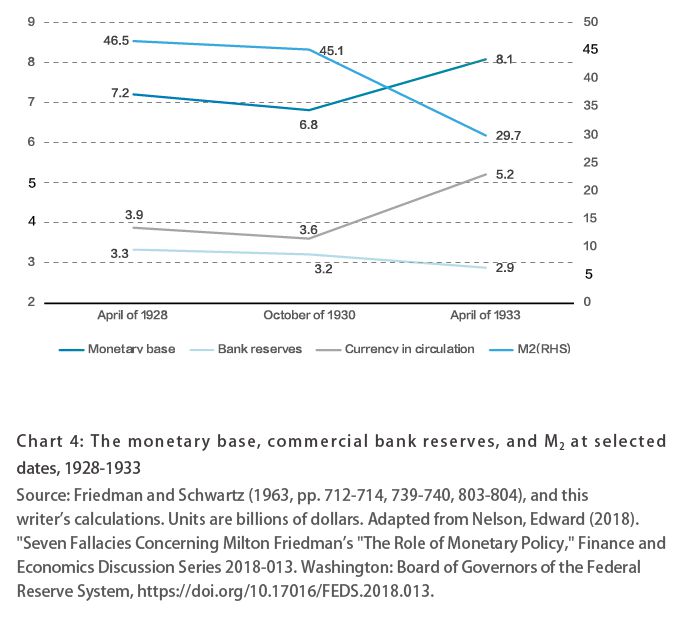

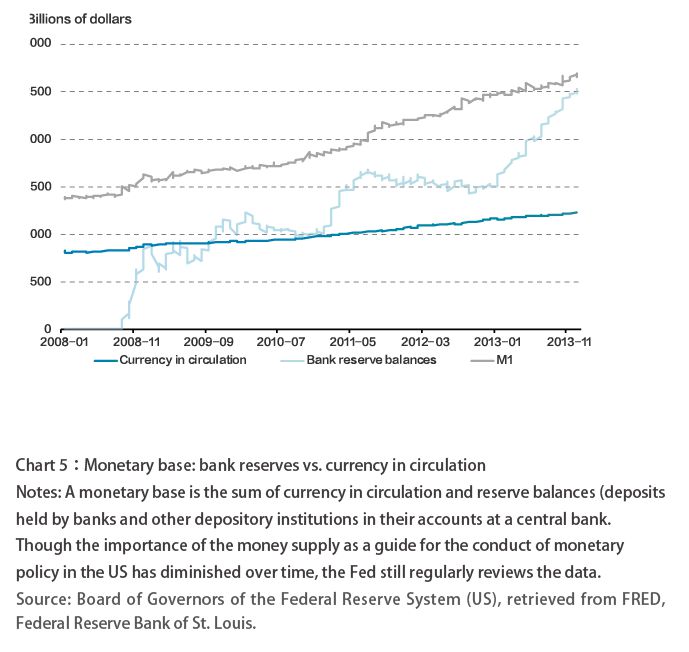

Nobel Prize-winner Milton Friedman stated that during an economic downturn’an increase in bank reserves is a good thing because it can stimulate the economy’presumably because that the increased bank reserves could be pushed into the stock of money. In his famous book "The Great Contraction’1929-1933"‘first published in 1963’ he believes that one of the important reasons why the Great Contraction was so severe and lasted so long was the sharp decline in the stock of money’and the main reason for the decline in the stock of money was that the Federal Reserve failed to effectively increase bank reserves (See Chart 4).

However’many scholars contend that this is far from satisfactory’especially in modern times. During a crisis’it is even more important to see a rise in the currency in circulation. Some studies have complained that this is exactly the problem that emerged during the 2008 financial crisis in the United States. The Fed's loose monetary policy increased bank reserves by more than 200 times in the five years to 2013’while currency in circulation rose slightly.(See Chart 4) Banks were reluctant to lend’and households and businesses did not want to borrow’thus limiting the role of monetary policy.

As Peter Temin (1976) and Paul Krugman (1998) pointed out’the pattern in Chart 4 also held in the Great Depression of the 1930s. As an economist who famously specializes in balance sheet recessions’Richard Koo (2012) showed that Japan witnessed a similar increase in bank reserves while currency in circulation remained constant from 1994 on’and the same holds true for major European countries during the Great Recession after the 2008 US financial crisis. In their important book House of Debt’Atif Mian and Amir Sufi (2014) strongly criticize central banks who were too heavily biased toward protecting banks and creditors "by flooding the banking system with reserves’but nobody wants to lend or borrow." (P156)

If these scholars see the sharp increase in currency in circulation’M1 and M2 in the past several months’they will probably be very happy and optimistic about the economic prospects after the pandemic. This means that the excess reserves get pushed into M1 and M2 and increase the currency multiplier’which is far more powerful than just the increase in reserves.

The Path to Recovery

But things are not that simple. There now are two diametrically opposed views: Some researchers expect that consumer spending will increase substantially’thereby promoting economic growth’and possibly cause inflation in 2021. The other camp says that due to the sharp upturn in unemployment’there is great uncertainty about when the pandemic will be controlled. People are hoarding money for unexpected needs’which may stifle the process of recovery.

The point of contention is actually: The economic recovery path in the future will largely depend on how people use the money they have been hoarding.

The author holds the second view. Currency in circulation’M1’and M2’have all increased significantly’which is indeed a positive sign. But because the unemployment rate remains high and the prospect of controlling Covid-19 worldwide is not encouraging’at least in the near term’the hoarding of cash is largely a preventive demand and will not turn easily to consumption. In addition’even if the pandemic comes under control’people's consumption behavior may not return to what prevailed in the past. This could be a drag on the recovery.

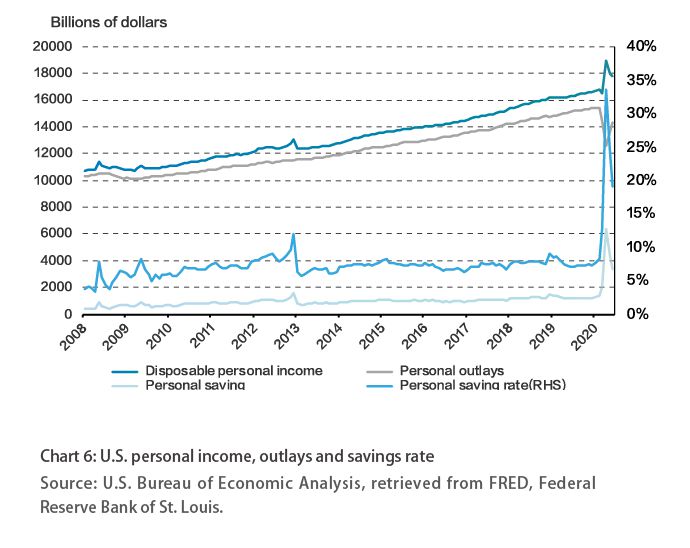

The change in the savings rate also demonstrates this point. The personal savings rate in the United States has hovered around 7.5% in recent years. In March this year’as the pandemic worsened’the savings rate jumped from February’s 8.4% to 12.6%. In April it surged to 32.2%. Although it dropped slightly in May’it was still a relatively high 23.2%. (See Chart 6) The savings rates of European countries are different from those of the US’but they also have been rising substantially. Not only is the personal savings rate climbing’but the corporate savings rate is also showing the same trend.

There is another reason for the hoarding of cash and it is related to the inconvenience – and increased risk -- of going to a bank or ATM during a pandemic. This is especially the case for low-income groups and minorities’which have been hit disproportionately hard by Covid-19. And in this segment of the public’there are many who do not even have a bank account.

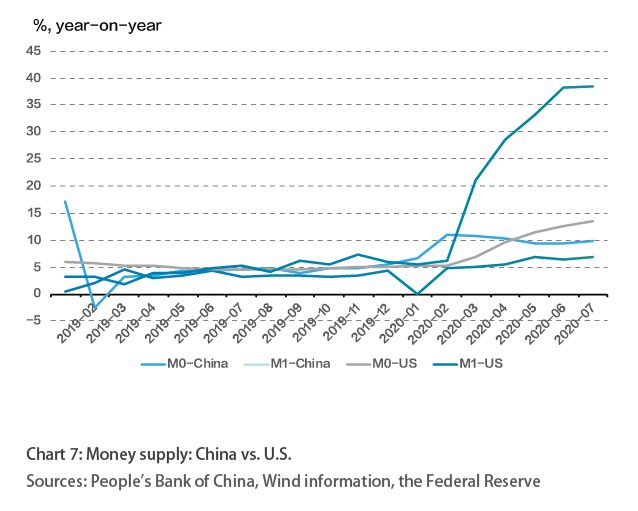

In any case’it is rare for the currency in circulation’bank reserves at central banks’and M1 to increase sharply at the same time. This is related to the forceful and aggressive actions of fiscal and monetary policy. The economic consequences of these actions will become apparent at some point in the future though they will have an extremely uneven regional distribution – both domestically and globally. This will depend on where the pandemic is effectively brought under control. At present’Europe appears to be better off than the United States. Although the growth rate of currency in circulation and M1 in China is relatively modest compared to developed economies’it still exceeds the normal levels prior to the pandemic (See Chart 7). Given that Covid-19 is already under control in China’there is much greater clarity on the prospects for economic growth.

The author is a visiting scholar at Harvard University and a former managing director at CITIC Securities